Navigating the world of motor insurance can sometimes feel like reading a foreign language. With various coverage options, policy terms, and potential penalties, it’s easy to get confused. To help you make an informed decision, we’ve broken down the key aspects of a standard Comprehensive or Third Party, Fire and Theft policy into simple, everyday language.

How Much Should You Insure Your Car For?

One of the most important decisions you’ll make is choosing your sum insured, the amount you want to insure your car for. Getting this number right is crucial, and it depends on whether you opt for a policy based on Market Value or Agreed Value.

Market Value vs. Agreed Value: What’s the Difference?

Understanding the distinction between these two valuation methods is key to knowing what you’ll be paid in the event of a total loss.

-

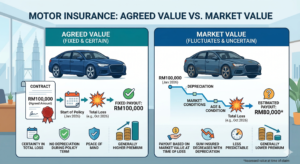

Market Value (Standard on Most Policies): Most standard comprehensive policies operate on a Market Value basis. This means the sum insured is not fixed. Instead, it fluctuates based on current market conditions. Think of it as the price it would cost you to buy an identical car, same make, model, age, and condition today.

-

The Risk: The main drawback is depreciation. If your car is stolen or declared a total loss, the payout is based on its value at that exact moment. Since cars depreciate over time, this amount is almost always less than what you originally paid for it. This can leave you with a shortfall if you still have an outstanding car loan.

-

-

Agreed Value (Often an Add-On): An Agreed Value policy allows you and the insurer to agree on a fixed sum insured for your car at the start of the policy period. This amount is locked in for the duration of that policy (usually one year) and does not depreciate.

-

The Benefit: The major advantage is certainty and peace of mind. In the event of a total loss, you know exactly how much you will receive: the pre-agreed sum. This is particularly popular for owners of modified cars, classic cars, or new car owners who want to protect themselves against the initial “drive-away” depreciation.

-

The Pitfalls of Getting It Wrong: Under vs. Over-Insuring

Whether you choose Market Value or Agreed Value, the amount you set (or the amount used to calculate your premium) must be accurate.

-

The Danger of Under-Insuring: This is a common pitfall with Market Value policies. If you set your sum insured too low (below the actual market value), you could be penalised when you make a claim. Insurers call this “average.”

-

Example: Let’s say your car’s true market value is RM100,000, but you only insured it for RM80,000. If you have an accident causing RM5,000 worth of damage, the insurer won’t pay the full amount. They will only pay a portion based on the shortfall.

-

The Calculation: (Sum Insured / Market Value) x Loss = Payout

-

(RM80,000 / RM100,000) x RM5,000 = RM4,000.

-

In this scenario, the insurer pays RM4,000, and you are left to pay the remaining RM1,000 out of your own pocket. This penalty typically applies if your sum insured is more than 10% below the market value.

-

-

The Waste of Over-Insuring: On the flip side, insuring your car for more than its market value is a waste of money. Your premium will be higher, but if your car is a total loss, the insurer will only pay out its actual market value at the time of the accident, not the inflated sum you chose.

The best way to protect yourself from under-insuring on a standard policy is to use a market valuation system approved by your insurer. For guaranteed payouts, discuss an Agreed Value add-on with them.

Understanding Your Policy Discounts and Costs

Two key terms that directly affect the price of your policy and your out-of-pocket expenses during a claim are No Claim Discount (NCD) and Excess.

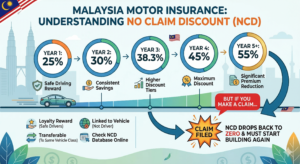

What is No Claim Discount (NCD)?

NCD is essentially a loyalty reward for being a safe driver. It’s a percentage discount on your premium for every year you don’t make a claim.

Below is a structured view of the data often found in policy spreadsheets to help you visualize your savings and potential costs.

| Years of No Claims | NCD Discount (%) | Potential Savings (on RM2,000 Premium) |

| 1st Year | 25% | RM500 |

| 2nd Year | 30% | RM600 |

| 3rd Year | 38.33% | RM766.60 |

| 4th Year | 45% | RM900 |

| 5th Year + | 55% | RM1,100 |

But beware one claim can reset your progress. If you or another authorised driver makes a claim, your hard-earned NCD will drop back to zero at your next renewal, and you’ll have to start building it up all over again. You can check your current NCD online through the Central NCD Database before purchasing a policy.

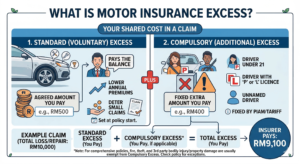

What is an “Excess”?

An excess is the fixed amount you agree to pay towards a claim. Think of it as your contribution. If you make a claim, you pay the excess amount first, and the insurer pays the rest.

-

Example: If you have a claim for RM10,000 and your policy has a standard excess of RM500, you pay the first RM500, and the insurer pays the remaining RM9,500.

Important Exceptions: The standard excess usually does not apply to claims like fire, theft, or third-party property damage and injuries.

Compulsory Excess: There is also an additional excess that may apply depending on who is driving. You will have to pay an extra RM400 if the driver at the time of the accident:

-

Is under 21 years old.

-

Holds a Provisional (P) or Learner (L) driving licence.

-

Is not named as an authorised driver on your policy schedule.

So, using the example above, if the driver was under 21, the total excess you’d pay would be RM500 (standard) + RM400 (compulsory) = RM900. The insurer would then pay the RM9,100 balance.

Who is Covered? Understanding “All Drivers”

It’s vital to know who is authorised to drive your car under the policy. While some policies are restricted to named drivers only, you can often opt for an “All Drivers” extension.

-

Named Driver Policy: Only you and the drivers specifically named in your policy schedule are covered. If someone not named drives your car with permission and has an accident, the claim might be rejected, or a compulsory excess may apply.

-

All Drivers Extension: This broader coverage allows any person to drive your car with your permission. This is a great option for families where multiple people might need to drive the car occasionally. However, be aware that the “young drivers” compulsory excess mentioned above will still apply if the driver is under 21 or on a provisional license.

Enhancing Your Coverage: Add-Ons to Consider

A basic comprehensive policy is a great start, but you can often add extra coverages for specific needs. Here are some common and valuable add-ons, including many that protect your passengers, your wallet, and your car’s most vulnerable parts.

Protection for You and Your Passengers

-

Legal Liability to Passengers (LLP): This is a critical coverage that is often included in a comprehensive policy. It covers your legal liability for bodily injury or death caused to any passenger travelling in your vehicle. In the event of an accident, this helps cover their medical expenses and potential compensation claims.

-

Personal Accident (PA): While LLP covers your liability to others, Personal Accident coverage provides a direct benefit to you and your family. It pays a fixed sum (e.g., up to RM50,000 per person) for accidental death or total permanent disablement for you and your passengers. This is separate from any third-party liability.

Protection Against Specific Incidents

-

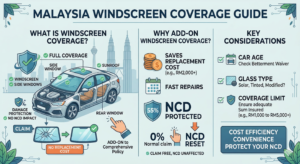

Windscreen and Glass Coverage: This is one of the most popular and practical add-ons. It specifically covers the cost of repairing or replacing your car’s windscreen, as well as other fixed windows and the sunroof.

-

The Key Benefit: Its biggest advantage is that you can claim for a cracked or shattered windscreen without affecting your No Claim Discount (NCD) . This means your premium won’t increase the following year just because a stray stone hit your windscreen on the highway.

-

What to Expect: Most policies cover the full cost of replacement at an authorised workshop, up to a reasonable limit. It’s a small add-on cost that saves you from a potentially large out-of-pocket expense and protects your hard-earned NCD.

-

-

Special Perils Coverage: This is one of the most important add-ons, especially in areas prone to unpredictable weather. Standard policies usually don’t cover “acts of God,” but this rider does. It protects your car against:

-

Floods: If your car is submerged in water.

-

Landslides and Landslips: Damage from moving earth.

-

Storms, Typhoons, and Hurricanes: Damage from high winds.

-

Earthquakes and Volcanic Eruptions.

-

Fallen Trees or Objects.

-

This coverage can be offered as “Full Cover” (up to your sum insured) or “Limited Cover” (e.g., up to 25% or 50% of your sum insured). It’s a relatively low-cost add-on (typically around 0.2% to 0.5% of your sum insured) that offers invaluable peace of mind.

-

-

Replacement of Car Keys: Losing your car keys can be a major inconvenience and expense. This add-on covers the cost of replacing lost or stolen keys, remotes, and transponders, often up to a limit like RM2,000.

-

Cleaning Cost of Vehicle: Following an event like a flood or an attempted break-in, your car may require professional sanitisation and cleaning. This add-on covers those cleaning costs, often up to RM5,000, ensuring your car is safe and fresh.

-

Compensation for Assessed Repair Time (CART): While your car is in the workshop undergoing repairs for a covered claim, you’re without a vehicle. The CART add-on provides you with a daily cash allowance (e.g., a fixed amount per day) to help cover alternative transport costs during this period.

Protecting Your Car’s Value and Parts

-

Betterment Buyback: This is a crucial add-on, especially for newer cars. When repairing your car, insurers typically use “betterment” meaning they deduct an amount for wear and tear on old parts being replaced with new ones. For example, if a 2-year-old tyre is damaged, the insurer might deduct a percentage for its usage before paying for a brand-new replacement. Betterment Buyback waives this deduction. The insurer covers the full cost of new replacement parts without penalising you for your car’s age or wear and tear.

By understanding these core principles the difference between market and agreed value, who is covered under your policy, how discounts and costs like NCD and excess work, and the wide array of available add-ons you can build a motor insurance policy that provides genuine protection and peace of mind on the road.