Samsung’s Five-Year Tax War: A Billion-Dollar Lesson in Estate Liquidity. What the Samsung Inheritance Saga Teaches Us About Planning

The recent news of the Samsung heir-apparents finally completing their staggering $8.6 billion (12 trillion won) inheritance tax bill is a wake-up call that reverberates far beyond the boardrooms of Seoul. It took five years, massive personal loans, and the offloading of significant company shares for the family of the late Lee Kun-hee to settle their debt with the taxman.

While most of us aren’t dealing with billions, the core lesson remains the same: Without a plan, your legacy can quickly become your family’s greatest liability.

The “Inheritance Trap”: A Legacy of Debt?

The Samsung saga highlights a terrifying reality of estate settlement. When a loved one passes, the government often expects its share in cash, and they expect it relatively quickly.

If your wealth is tied up in “illiquid” assets—like the family home, a private business, or sentimental heirlooms—your beneficiaries may find themselves “asset rich but cash poor.” To pay the taxes and legal fees, they might be forced into:

-

Fire Sales: Selling the family home or business under market value just to meet a tax deadline.

-

Crushing Debt: Taking out high-interest loans to cover the bill (as the Samsung family did).

-

Legal Warfare: Disputes between siblings over which assets to sell to cover the costs.

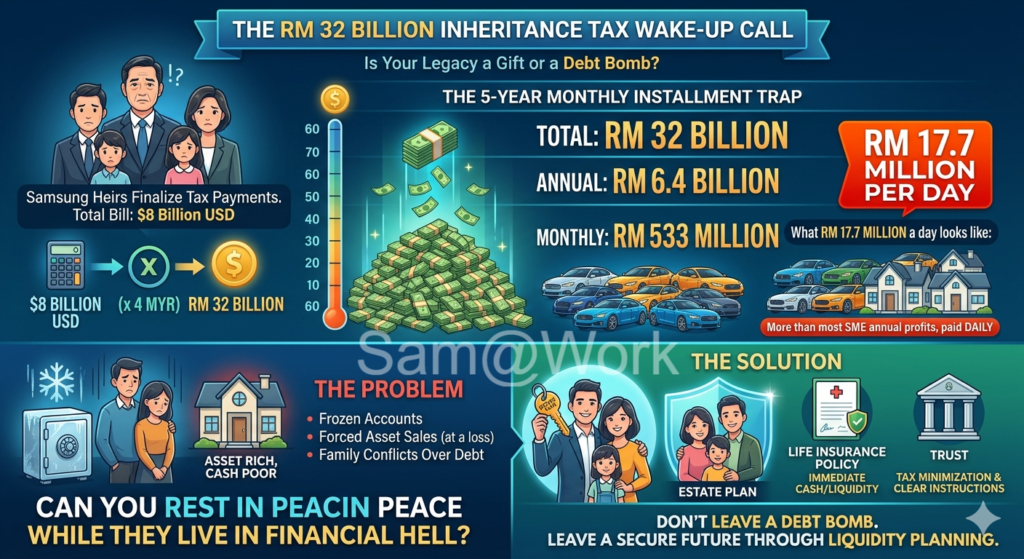

To put the Samsung family’s tax bill into perspective, let’s look at the sheer scale of the numbers when converted to Ringgit Malaysia (MYR) and broken down into manageable (or in this case, unmanageable) installments.

Based on the reported $8 billion USD figure, here is the breakdown using current exchange rates (approx. $1 USD = 4.00 MYR).

The Grand Total

The total inheritance tax bill is roughly:

$8,000,000,000 x 4.00 = MYR32,000,000,000(Thirty-two billion Ringgit)

The 5-Year Installment Breakdown

To manage this astronomical sum, the heirs utilized a 5-year installment plan (60 monthly payments).

Frequency Amount in MYR Total Bill RM 32,000,000,000 Annual Payment RM 6,400,000,000 Monthly Payment RM 533,333,333

Can You Rest in Peace While They Live in Hell?

The emotional weight of losing a pillar of the family is heavy enough. Adding a financial crisis on top of grief is a recipe for disaster. Estate planning is not about how much money you have; it’s about liquidity and logistics.

The “Living in Hell” Comparison

To put that RM 533 million monthly payment into perspective:

-

That is roughly RM 17.7 million every single day.

-

It is more than most successful SMEs in Malaysia make in an entire year—paid out every 24 hours just to keep the taxman at bay.

The Lesson: Don’t Leave a “Debt Bomb”

If the world’s most powerful tech family had to take out massive personal loans and sell off chunks of their “crown jewel” (Samsung shares) to meet these payments, what happens to a regular family when the breadwinner passes?

-

Frozen Accounts: In Malaysia, bank accounts are often frozen immediately upon death. Your family can’t even touch the money that is technically theirs.

-

The Cash Crunch: Lawyers, funeral directors, and creditors don’t wait for probate to be settled. They want their money now.

-

The Peace of Mind Solution: This is where Estate Planning and Liquidity Planning become the ultimate act of love.

-

Instead of leaving your children a bill for RM 500,000 and a locked house, you leave them something that pays out cash immediately.

-

That cash “unlocks” the estate, pays the lawyers, and ensures they can continue their lifestyle without interruption.

-

Your legacy should be a foundation for their future, not a weight that pulls them under. Plan your liquidity today, so they don’t have to pay for your success with their peace of mind.

The “Hell” Scenario

If you leave behind RM 10 million in property but RM 0 in the bank:

-

Frozen Assets: Your family cannot sell the house or withdraw money until the court grants probate.

-

The Cash Gap: They must pay lawyers and creditors out of their own pockets first.

-

The Forced Sale: They might be forced to sell your “dream home” at a 30% discount just to get the cash needed to settle the estate.

Why Estate Planning is Non-Negotiable

In Malaysia, while we currently do not have a formal “Inheritance Tax” (it was abolished in 1991), there are still significant costs that can paralyze an estate:

-

Legal & Probate Fees: Can range from 2% to 5% of the total estate value.

-

Real Property Gains Tax (RPGT): If the heirs need to sell property quickly to get cash.

-

Outstanding Debts: Mortgages, personal loans, and business liabilities that must be settled before heirs see a cent.

The Takeaway

If the owners of one of the world’s most successful tech empires had to struggle for half a decade to settle an estate, imagine the strain a lack of planning could put on your family.

Don’t let your final gift to your loved ones be a mountain of paperwork and a debt they can’t afford. Plan today, so they can grieve in peace tomorrow.

Samsung owner family to complete $8 billion inheritance tax payments this month.

Important: The information and opinions in this article are for general information purposes only. They should not be relied on as professional financial advice. Readers should seek independent financial advice that is customised to their specific financial objectives, situations & needs.

Published By:

Samantha Lim 林淑燕

Wealth Strategist | Will & Trust Specialist | Passive Income Architect

Most people work for their money. I design systems where money works for people.

With over 30 years in the financial industry and a background in Commercial Banking, I’ve learned that wealth isn’t built by just “saving”—it’s built by strategically deploying resources into the right tools at the right time.

I don’t just look at investments; I look at Resource Optimization. Whether it’s navigating complex market cycles or identifying high-performance assets, my approach is rooted in the same “Banker’s Rigor” I used to vet multi-million dollar corporate deals.

My Strategic Approach:

Tool Selection & Risk Management: Every financial tool has a purpose. I help you identify which “wealth machinery”—from high-yield dividends to strategic real estate or estate trusts—best fits your current life stage while shielding you from “invisible” risks like inflation and market volatility.

The Banker’s Due Diligence: I apply a institutional-grade vetting process to every opportunity. I look for the structural integrity of an investment—checking the “foundations” (legal, financial, and physical) before you commit your hard-earned capital.

Autopilot Systems: My goal is to help you architect a portfolio that functions as a self-sustaining ecosystem. I handle the complex structural engineering (Will, Trust, and Financing) so your income remains streamlined today and secured for tomorrow.

As Warren Buffett wisely said: “If you don’t find a way to make money work for you, you will work for money until you die.”

Wealth is not an accident; it is a design. Ready to architect yours?

Click HERE to start a chat!

财富策略师 | 被动收入架构师 | 前商业银行家

大多数人为钱工作,而我的目标是设计一个“让钱为你工作”的系统。

拥有超过 30 年的金融从业经验,并曾深耕商业银行领域多年,我深刻理解:财富的增长不仅仅靠“存钱”,更取决于你是否能在正确的时机,将手头的资源配置到正确的“工具”中。

我不只是在看投资机会,我更是在做资源优化(Resource Optimization)。无论是应对复杂的宏观经济周期,还是筛选高表现资产,我的方法论始终植根于我在银行审核千万级企业贷款时所秉持的**“风控严谨度”**。

我的战略逻辑:

工具筛选与风控: 每一种金融工具都有其特定用途。我帮你识别哪些“财富机器”——从高股息组合、战略性不动产到家族信托——最契合你当前的人生阶段,同时帮你抵御通胀与市场波动带来的“隐形”风险。

银行级别的尽职调查: 我将机构级的风控流程应用于每一个机会。在投入你的血汗钱之前,我会先用“银行家之眼”透视其结构完整性——从法律合规、财务透明到底层资产的真实性。

自动导航系统: 我的目标是帮你架构一个能够自我运作的资产生态系统。我来处理复杂的底层设计(包括融资架构、遗嘱与信托的闭环),让你不仅拥有现在的现金流,更拥有未来的确定性。

正如巴菲特所说:“如果你没法在睡觉时赚钱,你将工作到死。”

财富不是偶然发生的,它是被设计出来的。准备好开启你的财富架构之旅了吗?

咱们聊聊吧!点击【这里】直接开始对话!